Laura du Preez | 14 March 2023

Laura du Preez has been writing about personal finance topics for more than 20 years, including eight years as personal finance editor for two leading media houses.

The outlook for the South African economy may be dire, but the same is not true for its financial markets, asset managers say.

Many have moved some more of the money they invest for you offshore, but they are not quitting South African markets as much as they could have and they don’t think you should either.

Last year financial markets delivered poor returns to investors around the world.

|

|

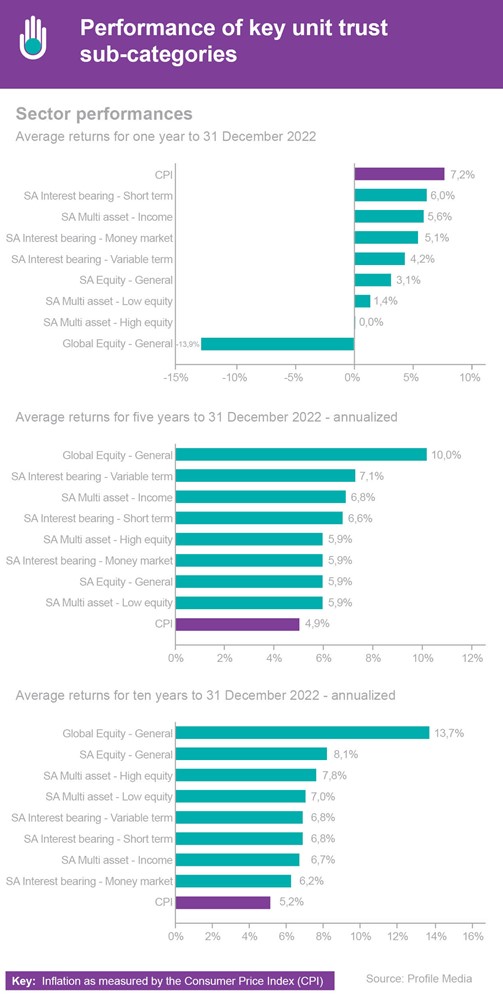

The annual average returns of the unit trust sectors show how difficult 2022 was for investors across all asset classes in local and offshore markets. Average returns over longer terms, however, show investors have been rewarded in line with the risk of their investments and have beaten inflation, Sunette Mulder, senior policy adviser at the Association of Savings and Investments, said when releasing the association’s latest statistics. |

Investors in unit trusts invested in offshore markets were down on average close to 14%.

South African equity unit trusts, however, delivered on average 3% for the year, according to Profile Data.

The nominal return for shares on the JSE was 3.8%, Debra Slabber, portfolio manager at Morningstar told the recent Investment Forum. This was not “earth-shattering”, but it was better than the nominal return for shares on other emerging markets, which showed a loss of 14.4%. Globally share markets, as measured by the MSCI World index, were down 12.74%, she said.

The Investment Forum conference is organized by the Collaborative Exchange and is held annually in March in Cape Town and Johannesburg.

In the local market, loadshedding was a big killer, but it should not lead you to make emotional decisions about your money, Malcolm Charles, portfolio manager at Ninety-One told the conference.

Some companies are still making money for investors, he said, citing FNB which has delivered a return of 16% a year since 2016 when the extent of state captu

re became more evident.

A bit more offshore

Last year the offshore limit for managers of South African funds was raised from 30% to 45%, but managers of leading multi-asset funds have been cautious in increasing their offshore allocations.

M&G has taken the offshore exposure of its Balanced Fund from 25% to 29% over the past year.

Leonard Krüger, the co-manager of the fund, told the Investment Forum that “we are just finding more opportunities for decent risk-adjusted returns in South Africa”.

Krüger said M&G’s research has also shown that it is not optimal to take offshore exposure for a South African investor well beyond 35%, as the currency exchange rates introduce volatility.

Rory Kutisker-Jacobson, co-fund manager of the Allan Gray Balanced fund, agreed that an offshore exposure of 35% is the right amount now but may in the future take the fund’s offshore exposure between 30% and 45%, depending on the opportunities.

It is relatively early to understand US inflation and whether it will be transient or persistent, so Allan Gray is investing its offshore allocation in shares and other securities outside of the US, he says. Read more: Do unit trusts invest in financial markets outside of South Africa?

Check cycles

The PSG Balanced Fund upped its offshore exposure from 28% to 35% of the fund over the past year.

Justin Floor, the co-manager of this fund, says it is important to take the temperature of certain cycles before you move money offshore.

The first one is the level of the dollar relative to where it should be, and “we are not piling into potentially a very expensive dollar”, Floor says.

The first one is the level of the dollar relative to where it should be, and “we are not piling into potentially a very expensive dollar”, Floor says.

You also need to take the temperature of the commodity cycle, he said.

There has been a decade of deep underinvestment in commodities and the focus on environmental, social and governance issues is increasing demand for certain commodities required for clean energy, such as wind and solar power.

The result is much higher commodity prices and probably favours commodity-exporting countries like South Africa, he said.

Prices relative to earnings matter

Floor said PSG practices bottom-up investing taking into account the valuations of the shares and other securities it picks. The currency risk of the fund is then managed by favouring shares that are not dollar-denominated like those listed in Europe and the UK.

It is good to have offshore exposure as it gives you good diversification away from South African market risks which are real, but you should not invest at any cost, he said.

It is good to have offshore exposure as it gives you good diversification away from South African market risks which are real, but you should not invest at any cost, he said.

PSG still has a 40% exposure to local equities in its balanced fund, M&G has 46% and Allan Gray has 52%, although this includes hedged equities and commodities.

| LEADING MULTI-ASSET FUNDS ASSET ALLOCATION | |||

| Asset class | PSG Balanced | M&G Balanced | Allan Gray Balanced |

|---|---|---|---|

| SA Equity | 40% | 46% | 52%* |

| Foreign Equity | 31% | 24% | 28%* |

| SA Bonds | 20% | 20% | 8% |

| Foreign Bonds | 2% | 4% | 4% |

| SA Property | 3% | 2% | 1% |

| SA Cash | 2% | 3% | 5% |

| Foreign Cash | 1% | 1% | 2% |

|

*Including commodities and hedged equity |

|||

Krüger says M&G still has substantial exposure as you are still being well compensated for taking risks in South Africa despite all the macro-economic problems.

He says while 2022 was a disaster for international investors who lost 15 to 20 % in equities and bonds, this was not the case for SA because our starting prices were very different compared to expensive global shares and bonds.

The valuations protected you, he said. Read more: What are the investment styles a manager can follow?

SA equities not all equal

Slabber said some local shares are offshore earners and less affected by the local economy.

Others, like the resources shares, will be driven by increased economic activity in China following its Covid lockdowns. Naspers, meanwhile, with a large holding in Chinese tech stock Tencent, will be influenced by the Chinese government’s interventions in technology companies and share structures.

Larger managers like Allan Gray tend to have higher exposures to large offshore earners, while smaller managers can have greater exposures to small and mid-cap shares with exposure to the local market. These are known as SA Inc shares.

SA Inc shares resilient

Managers agreed SA Inc companies that survived the past difficult decade were remarkably resilient but despite this, the market had not priced them higher.

Rob Spanjaard, chief investment officer at Rezco, said there is great value in small- and mid-cap shares and the price is right even if the economic outlook is weak.

Rob Spanjaard, chief investment officer at Rezco, said there is great value in small- and mid-cap shares and the price is right even if the economic outlook is weak.

Spanjaard said it was good to back innovators – the likes of Discovery, Aspen and Bidvest.

Krüger said these companies have not been expanding so they have cash to spend on coping with loadshedding.

Neville Chester, portfolio manager at Coronation, said what companies do with that cash will determine who the winners are in the future. The winners will take from their competitors rather than from consumers who are under pressure, he said.

The equities panel debated, but downplayed, the risk of a total collapse of the electricity grid.

Spanjaard, Wim Murray from Foord and Jacques Conradie from Peregrine Capital, agreed that the fact that South African companies have the capital and the skills to fix the energy crisis in South Africa would ensure good business for a lot of companies.

What is a unit trust fund?

What kinds of unit trusts are there?

Why are there different kinds of multi-asset funds?

Do unit trusts invest in financial markets outside of SA?

How can I invest safely offshore?

What should I consider when investing offshore?

What are the investment styles a manager may follow?

Do you understand investment management speak?

Investment markets are complicated, but you can still make money

Fund classification tool