-

What you need to know before tax season 2026 begins

-

The healing journey from wounded to wealthy

-

Aspire to earning a passive income with a realistic plan

-

Why do-it-yourself (DIY) investors often need to seek advice

-

Rights for dads result in reduced maternity benefits for mums

-

Small money, big future: how investing in your 20s pays off

-

Who pays for the damage to my car from an accident that wasn’t my fault?

-

Finfluencers, AI and the new advice gap: how to protect yourself

-

Black tax: The fine line between helping and enabling

-

The electric car you think you can’t afford might actually cost you less

-

Why saving feels harder than ever

-

Don’t let past decisions trap your future wealth

-

Naming the money traumas shaping South African lives

-

How to make inheritances for overseas heirs simple, fast and tax smart

-

Umbrella trusts, beneficiary funds can help with the care of elderly dependants

-

ConCourt decision nullifies contracts couples sign after customary marriages

-

What I wish I had known before my first payday

-

Insurance shows up in real-life odds of thriving after a cancer diagnosis

-

Tax certainty for unit trust, retail hedge fund investors

-

The five hidden struggles of black tax – and how to take your power back

-

A quiet change that makes a big difference to small businesses

-

JSE’s concentration of large shares crowds out diversification

-

Why investment managers are turning to unlisted markets

-

Why diversification still matters, especially when one market is winning

-

Stay ahead of the class on fees and school extras

-

Where to focus when markets are volatile

-

Boom or bust: navigating AI in the markets

-

Why your manager probably lagged the market last year

-

The R15m exemption and why timing your business sale matters more than ever

-

The “quiet” financial wins: boring habits that outperform clever ideas

-

Understanding money wounds and their impact on our financial lives

-

Budget gives taxpayers a little breather

-

VAT threshold relief for small businesses and contractors

-

What true loves share without losing each other

-

Money anxiety in a world that never switches off

-

Financial blind spots you should try to avoid this year

-

The hidden cost of cheap financial advice

-

Are funds out of fashion? Should you invest directly in the market?

-

Separating after decades: coping with grey divorce

-

Betting on the right financial strategy

-

2025’s lessons in retirement income planning

-

Are insiders behind SARS eFiling hijackings?

-

Understanding how financial planners are paid

-

Watch out for dangerous financial advice from finfluencers

-

Leveraging social media to sell overseas

-

How you can build trust, wealth and harmony as a couple

-

How safe are my personal documents in the cloud?

-

Tweak your existing investments only if it furthers your goals

-

Is pet insurance worth it?

-

What to do if you have a big life and disability cover gap

-

Sports betting: wager or wise strategy?

-

Experts urge Muslims to plan for Shariah-compliant estates

-

How financial projections can secure small business funding

-

Curiosity – A key ingredient for financial health

-

Where there’s a will there’s a way

-

Strategies for effective wealth transfer

-

The big four financial decisions

-

Unintended consequences of tariffs could see US falter as market darling

-

Emerging markets set to benefit from shift from west to east

-

Make sure you sign your will with a pen

-

We could all retire better if …

-

Your savings pot can boost your financial position or cost you dearly

-

Will an inheritance affect my income protection payments?

-

Should you diversify across managers with different investment styles?

-

Failure to increase VAT threshold burdens small businesses

-

Expect tax certificates for cryptocurrency transactions soon

-

Double or nothing: double down on marketing your small business now

-

The architect, builder and repair man of your financial house

-

Insurance lessons from the ombuds

-

Keeping up with appearances - the wealth drain

-

Inside a cyberattack: a small business owner’s lessons from the frontline

-

Your insurance policy is not your maintenance plan

-

Mastering your money: seven key principles to keep cash flowing

-

It is tax season again - what should you look out for this year

-

When the seas are rough, repair your nets

-

Are you betting on US equity markets continuing to outperform the rest of the world?

-

Building financial confidence starts when your children are young

-

Understated expenses may explain why so many can’t afford repayments

-

The power of investing early and how to catch up if you are a late starter

-

Saving on medical scheme contributions for young adults

-

Who pays my medical expenses when I am in a road accident?

-

Treasury - A fancy word for the cliché “Cash is King”

-

Can you be overinsured with funeral policies?

-

President to appeal NHI challenge in ConCourt

-

Factors to consider when purchasing a retirement home

-

Risk rating creeps back into healthcare cover

-

Who will SARS target for an additional R800 billion in tax?

-

Use your entrepreneurial mindset to scale business amid political uncertainty

-

Connection – The fuel that drives the engine of financial advice

-

Credit regulator’s new guidelines bring relief for financially distressed consumers

-

The hidden price tag on your dream home: What banks won't tell you

-

A case study of challenges faced by SMEs in South Africa

-

How investors can be at peace amid market chaos

-

The future of investing: broader exposure without platform fees

-

Does your password protect your savings and investments?

-

The insurance lesson from a stolen phone at a cricket match

-

Clarity – The cornerstone of financial health

-

Multi-asset managers balance the risks to earn above-inflation returns

-

A smoother investment ride may enhance your returns

-

Revised budget will take R28 billion from us in VAT and income tax bracket creep

-

The dangers of falling for the AI market hype

-

Don’t make assumptions when it comes to providing for your minor children

-

SA equity funds moving back up average in return rankings

-

Ways to log your business trips for a tax deduction

-

Family business as usual in unusual times

-

Could we still see a hike in VAT when the budget is tabled?

-

Ground rules for students funded by the bank of mom and dad

-

Mistakes people make when asking for a salary increase

-

The will from hell – why professional advice is essential

-

The wisdom of not mixing business with pleasure

-

If you work abroad as an SA resident you may enjoy a tax exemption

-

Adulting gets easier when you know how to go about saving and investing

-

Ways to manage withdrawals from a living annuity

-

How you can get financially healthy

-

Five new year’s resolutions for a better financial life in 2025

-

Tax lessons we learnt in 2024

-

What we learnt from the markets in 2024

-

Small business lessons we learned in 2024

-

Why disability and severe illness policies are often so difficult to understand

-

Medical scheme networks can save you if you follow the rules

-

Dezemba is here

-

Path of least resistance to NHI: a 4% tax for healthcare free-riders

-

Are you getting retirement benefits counselling early enough to ensure you retire in comfort?

-

Why some members didn’t get savings pot withdrawals quickly

-

Stay balanced this Black Friday

-

Protect your income when you need it most

-

Franchises better positioned to succeed

-

Discretionary investments - your safety net for unexpected costs

-

New unit trust categories make it easier to find funds investing only in SA

-

Get some tax advice before you work your way around the world

-

Don't worry about the world, just save enough for your retirement - Fink

-

South Africans pay R40 billion for denied medical scheme claims - are you one of them?

-

How to spot a fake financial services company

-

Why are passive funds more popular in the US than in SA?

-

Your brain may need to be managed when it comes to money

-

Say no to (savings) pot

-

Legislation to support people living with dementia is still missing in SA

-

If you have minor children, be sure your will has these provisions

-

Pre-authorisation does not mean your scheme will pay your bills

-

Even after death: Costs. Costs? Costs!

-

Use the two pot system wisely and reach all your goals

-

How an enterprise and supplier development programme could help your SME

-

Why procrastination costs you twice

-

Life insurance pays, but only by the rules

-

How profit and purpose are enmeshed in investing

-

Are you avoiding making a plan for your retirement?

-

Small steps, big results: building wealth on any income

-

You, SARS and your duty to declare and pay tax

-

Don’t believe FX trading sites’ get-rich-quick hype

-

The tricky job of managing a living annuity through retirement

-

Two pots: Insufficient funds, tax and other hurdles facing members who want to withdraw

-

How you can live a rich life

-

Two-pot retirement system: why advice is so important

-

Offshore remains best return target while local risks should be managed

-

It's a wild world – there’s a lot of bad out there so beware

-

Is it time to give money its rightful role in your life?

-

Digital tools help small businesses master their money

-

Schemes get costlier as reform takes back seat to NHI

-

Why life cover is crucial for young families

-

Why schemes will contest the NHI Act now that it is signed

-

Play to win: the five-step process to winding up an estate

-

Two-pot retirement system: don't just focus on the cash

-

Employers pay arrear retirement contributions after shaming

-

Can’t get no satisfaction? It is getting easier to complain to an ombud

-

Do these financing models suit your business?

-

Don’t be a fool this April

-

A small business survival kit for tough economic times

-

Swix indices on the way out as JSE simplifies benchmarks

-

Diversify your investments as managers disagree on global equity outcomes

-

Expect multi-asset fund returns to diverge further in future

-

10 traps to avoid with buy-and-sell agreements

-

Keith Engel: only one way to stop average tax rates rising

-

More tax from you will plug the hole in the national budget

-

Effective tax planning saves SMEs time and money

-

Six financial planning tips for DINKs

-

Is love enough to bridge a money gap?

-

Tax year-end alert: Have you maximised your tax deductions?

-

Expect inflation-beating returns amid a noisy year in investment markets

-

Palesa Dube's lessons learnt as an entrepreneur

-

What happens to your retirement savings when you emigrate?

-

Savings hacks: Four New Year’s resolutions for new entrepreneurs

-

Living annuity drawdown rate is personal

-

Investing: Should you DIY, take advice or something in between?

-

Don’t be a victim of investment fraud - be vigilant all the time

-

Small business, big decisions: mastering the art of financial decision-making

-

The personal finance lessons we can all learn from 2023

-

Active ETFs have arrived in SA – should you care?

-

One of your most important financial decisions is the partner you choose

-

Two pots – don’t bank on getting access to your money in March

-

How to get creditworthy when you don’t have credit

-

Three top financial habits of successful entrepreneurs

-

As citizens of the world, South Africans need more specialised advice

-

Enjoying the holiday season without a budget blowout

-

Minimising the hidden retirement cost of maternity leave

-

Greater need for fairly priced pensions

-

10 tips for a bulletproof business plan

-

Tweaked two pot system likely to be delayed

-

Can money play a spiritual role in your life?

-

How to deal with medical scheme contribution increases and benefit reductions

-

When life cover starts costing an arm and a leg

-

How you can recoup some expenses for learning difficulties

-

How to choose the right capital structure for your small business

-

How much equity exposure will ensure your retirement income grows?

-

Unlocking financial freedom in seven micro steps

-

Challenges at the Master of the High Court for deceased estates

-

Planning your money around your life

-

How financially literate are you?

-

How small businesses can master financial planning

-

A special reminder to women to consider the “what ifs”

-

With a little knowledge and confidence, you too can be a great investor

-

Too many choices may be increasing your anxiety

-

The pitfalls of investing in buy-to-let property

-

Unpacking the four-letter word: debt

-

How to make money

-

Cash flow is the key to keeping small businesses afloat

-

An increase in your earnings could kickstart your savings

-

The savings KISS - keep it separate and simple

-

The value of a financial planner

-

What should you do if you inherit a firearm?

-

Saving & Investing: Some lessons from history

-

Filing the correct tax return is your responsibility

-

How your grief case and other baggage is a drag on how you manage money

-

The new global investment reality

-

Keeping-it-simple diversification

-

Guaranteed pensions offering best rates in a decade

-

7 things you should know about the latest two-pot retirement proposals

-

You can improve your retirement income with the right decisions

-

When costs keep rising

-

Get legal help if you wish to bequeath rights to property

-

Hundreds of thousands of taxpayers hit with penalties for outstanding returns

-

Public and private health care remain broken as we await grandiose NHI

-

Retirees with multiple incomes need to carefully consider SARS tax directives

-

Employer short-paying retirement fund ordered to make good

-

New measures to stop employers from failing to pay retirement fund contributions

-

Do I need a financial adviser?

-

Home equity release: shady scheme or lifesaver?

-

Trading platforms - where scamsters love to hide and other high risks

-

Do you understand the ins and outs of your marriage contract?

-

Contributing regularly gives you the benefit of rand-cost averaging

-

When life happens … are you anchored?

-

Retirement fund death benefits aren’t a right for the nominated

-

Homeowners need to be prepared for interest rate hikes and other costs

-

Bursting the bubble and other myths about passive investing

-

Volatility sees more investors diversify with hedge funds

-

Things are bad in SA, but managers are still choosing local

-

How are Retirement Fund excess contributions treated in retirement?

-

Choosing to live child-free puts a new focus on your financial plans

-

What will bracket relief save me in tax?

-

What does the 2023 Budget mean for your finances?

-

Opposites attract but can love conquer all?

-

Do you need to buy or top up a retirement annuity?

-

What can you do if your retirement annuity is worrying you?

-

Instant wealth's allure often has hellish consequences

-

Match your new year goals to your budget

-

Look after your mind, wallet and soul this festive season

-

Christmas gifts for children that keep on giving

-

How to get good value from your medical scheme

-

Delays in winding up estates continue

-

Why you need to be alive to changes in your group life cover

-

Don't let black put you in the red

-

Should you use buy now, pay later credit?

-

Property can be a great investment until it goes pear-shaped

-

Recession looms but offshore investors’ pain may ease

-

It’s a real risk to have a large gap in your life cover

-

How to plan a career break to pursue an adventure of a lifetime

-

Focus on things that matter for your financial well-being

-

Crypto assets are now financial products – what does that mean?

-

Why social media is not the place for solid financial advice

-

Does the taxman need to know about your side-hustle?

-

The real-life financial horror story

-

How not to get scammed when you try get out of debt review

-

Beware the will that is too simple for your affairs

-

Can you claim a home office tax deduction?

-

Help your child spend their allowance effectively

-

Don't let being the nurturer disempower you financially

-

This should make sense even at age 25

-

Planning for retirement and a good chance you will live to 100

-

Take care when choosing a tax practitioner

-

It's Savings Month: just start

-

Inflation - and interest rates - will things get worse before they get better?

-

The worst investment decision you can make

-

Paying for financial advice: fees on investments or professional fees in rands?

-

Life policy and investment proceeds worth R33.5bn unclaimed

-

The tax savings many retirees miss

-

Investment markets are complicated, but you can still make money

-

Hard-earned money grows faster in a tax-free savings account

-

Get ready, tax filing season is coming

-

Finding a good manager – is high conviction the key?

-

Survive the cost of living crisis – what you need to do now

-

Balloon payments are no party

-

A deathly get-rich scheme you do not want to be part of

-

More tax on my pension – can that be right?

-

How much offshore exposure should you have?

-

The investment grass isn’t always greener on the other side

-

Keep your goals in sight as markets react to Ukraine and other threats

-

Retirement funds can invest more offshore now but many are likely to take their time

-

Learning years ahead? Take some lessons on how to lighten the school fees

-

A little relief for South African pockets

-

Retirees on more than one pension should expect more tax to be withheld from March

-

Valentine’s Day trigger a money moment?

-

Be my Valentine, and ask me anything about my budget

-

More rights for life partners, but it still pays to protect yourself

-

Watch out for penalties as tax return deadlines come and go

-

Be more mindful about your money in the new year

-

Home insurance claim rejected for wear and tear. Is that fair?

-

Investors continue to move offshore

-

How to be sure your life insurance will pay out

-

Don’t be led into holiday season temptation

-

Covid reinforces the need for income protection for shorter illnesses

-

Despite lower medical scheme increases, your cover may still need a check up

-

Scheme increases below salary increases on average, but it may still be a heavy dose

-

Finding a suitable investment - conservative or aggressive is not enough

-

New proposals could give dismal pension numbers a big boost

-

The cost of not getting advice

-

Thinking of raiding your retirement savings? Think small and think twice

-

Choosing a pension more about blending than choosing one over the other

-

Will your family finances survive the loss of a breadwinner?

-

Investors losing out on growth with fund choices

-

How to cope in tough times

-

It's a really bad time to die without a will or an estate plan

-

Beware the man-in-the-middle of your transaction emails

-

Tax return deadline looms with penalties for those who miss it

-

All you need to know about two-pots and retirement

-

Is it a good time to buy your first home – or should you wait?

You can improve your retirement income with the right decisions

Laura du Preez | 08 June 2023

Laura du Preez has been writing about personal finance topics for more than 20 years, including eight years as personal finance editor for two leading media houses.

More than 70% of consumers surveyed for this year’s Sanlam’s Benchmark Retirement Survey are concerned about not having enough money for retirement.

It is never too late to do something about shortfalls in your retirement savings, but you need to be engaged and appreciate the implications of your choices if you want to improve your future income.

It is never too late to do something about shortfalls in your retirement savings, but you need to be engaged and appreciate the implications of your choices if you want to improve your future income.

Releasing this year’s survey, Sanlam’s retirement industry professionals highlighted that one of the biggest choices you need to make is to preserve your savings – ideally all of it – even after the two-pot system comes into place and allows you to withdraw some of your savings.

South Africans withdraw their retirement savings – often all of it - too often when they change jobs, resulting in less than 10% of members being able to maintain their standard of living when they retire, Lorraine Mekwa, the managing director of client experience at Sanlam Corporate, said at the release of the survey this week.

Two-pot will be significant

This will no longer be possible after the two-pot system is introduced, which will have a significant effect on savings - mostly for younger members, Marian Gordon, the principal investment consultant at Simeka Consultants & Actuaries, said.

Under the two-pot system, one-third of what you contribute to your retirement fund will be held in a savings pot from which you can withdraw once a year.

Under the two-pot system, one-third of what you contribute to your retirement fund will be held in a savings pot from which you can withdraw once a year.

Despite the withdrawals being allowed, the remaining two-thirds of what you save in your retirement pot will have to be preserved until retirement and you will not be able to access this money when you change jobs. Read more: What is the two-pot retirement savings system?

The forced preservation of the retirement pot will have a significant effect on members’ retirement savings, Gordon said.

The numbers prove it

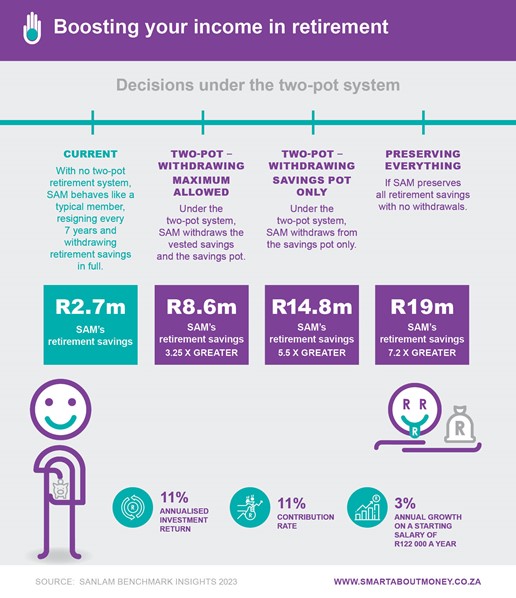

She illustrated this with the example of a member who starts saving at 20 and by age 24 is earning R122 000 a year and has saved R85 000 by contributing 11% of her salary to her fund.

Let's call the member Sam. Gordon said if Sam, like most current retirement fund members, changes jobs every seven years until age 50, and each time she withdraws all her savings, when she retires at age 65, she will only have R2.7 million saved.

Let's assume the two-pot system is implemented when Sam is 24 years old, she won’t be able to withdraw all her savings - she will only be allowed to withdraw the one-third she saves in future. She will also be able to withdraw the R85 000 she had already saved when the system was introduced, known as her vested savings. Despite making these withdrawals, she will still retire significantly better-off with R8.6 million – in excess of three times more.

Let's assume the two-pot system is implemented when Sam is 24 years old, she won’t be able to withdraw all her savings - she will only be allowed to withdraw the one-third she saves in future. She will also be able to withdraw the R85 000 she had already saved when the system was introduced, known as her vested savings. Despite making these withdrawals, she will still retire significantly better-off with R8.6 million – in excess of three times more.

If Sam, does not withdraw the R85 000 she has saved so far, and in future only withdraws the one-third she saves into the savings pot, she will retire with a sum of R14.8 million.

If, however, she chooses not to access either her vested savings or the savings pot, and preserves all her savings until retirement, she could retire with R19 million – more than seven times what she will have if she keeps withdrawing every seven years, Gordon says. Read more: How much do I need to save for retirement?

Withdrawals will hurt you

The example shows how important it is to consider the impact of any withdrawals you make from your retirement savings.

The two-pot system has the potential to deliver on its two objectives of providing access to savings in emergencies and funding an income in retirement, Mekwa says.

The two-pot system has the potential to deliver on its two objectives of providing access to savings in emergencies and funding an income in retirement, Mekwa says.

But there are more pitfalls for members. The danger is that members will treat the savings pot of the two-pot system as a bank account that can be used for frivolous things, and that will be detrimental to their future, she says.

The Benchmark Survey research shows that 38% of members withdraw their retirement savings to fund lifestyle costs. Read more: Why is withdrawing from my retirement fund a bad idea?

Members need to be empowered to explore their choices without hampering their future long-term retirement outcomes. Making use of counselling and financial advice will be key, Mekwa says.

Preserving needs to start early

Mekwa says while the two-pot system will help younger members, it can’t save older members who have not preserved. She said that in contrast to Sam’s case, a member with the same earnings and savings rate as Sam, but who is 51 when the two-pot system is introduced, will experience a much smaller benefit from being forced to save what is in the retirement pot.

The member who has been cashing out every seven years, and continues to withdraw what he contributes to the savings pot, will reach retirement with only R1.4 million saved.

The member who has been cashing out every seven years, and continues to withdraw what he contributes to the savings pot, will reach retirement with only R1.4 million saved.

Older members can, however, improve their retirement savings by not accessing the money in the savings pot when the new system gives you the option to do so, Mekwa says.

Saving more for growth

Older members should also consider making additional voluntary contributions to boost their retirement income and should ensure that their savings are invested optimally.

Anna Siwiak, head of product solutions for Sanlam Umbrella Solutions, says the Benchmark Consumer Survey of 600 retirement fund members shows that many (44%) do not engage with how their savings are invested after joining a fund.

Anna Siwiak, head of product solutions for Sanlam Umbrella Solutions, says the Benchmark Consumer Survey of 600 retirement fund members shows that many (44%) do not engage with how their savings are invested after joining a fund.

A good financial adviser will help you to plan your retirement. Read more: What should I think about when planning my retirement savings?

If you are not on track to get the income you need in retirement, consider saving more. Member data from the Sanlam Umbrella Fund shows that more than 30 000 members out of more than 300 000 are making voluntary additional contributions to their funds. Many (57%) are over the age of 50.

They typically contribute 5% of their salaries in additional contributions, but some contribute as much as 28%, often as a lump sum from, for example, a bonus. Find out how much more you can contribute and enjoy a tax deduction: Tax deductible retirement fund contributions

Stressing or saving

Koketsho Mahlalela, head of member-led outcomes at Sanlam Corporate, says the consumer survey showed more than 50% of consumers would contribute more to their retirement funds if they could.

But almost two in three are stressing about their financial situation and only 20 percent of respondents believe they are getting advice early enough in their lives to improve their finances. Read more: How can I find a good financial adviser?

But almost two in three are stressing about their financial situation and only 20 percent of respondents believe they are getting advice early enough in their lives to improve their finances. Read more: How can I find a good financial adviser?

This could mean that people are living with an extended period of anxiety, not knowing how or what to even think regarding their financial futures, Mahlalela said.

Related topics

How much do I need to save for retirement?

Why is withdrawing from my retirement fund a bad idea?

What should I think about when planning my retirement savings?

How can I find a good financial adviser?

Related hot topics

New proposals could give dismal pension numbers a big boost

Planning for retirement and a good chance you will live to 100

Related tools

Tax deductible retirement fund contributions